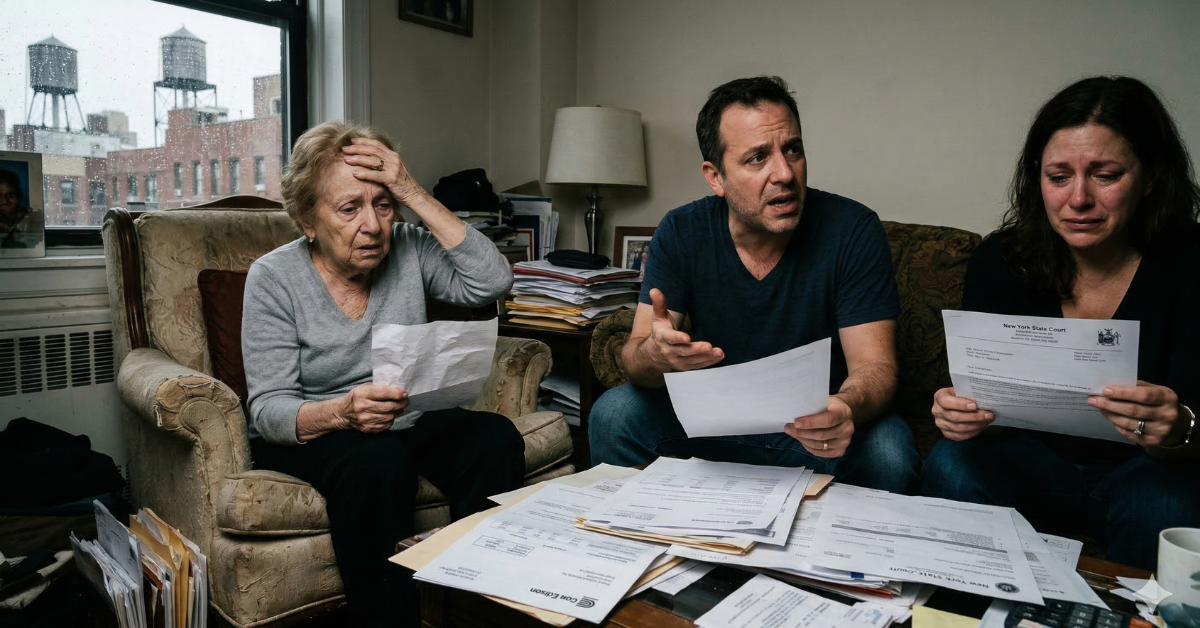

Most families never see it coming. Not really. There are signs: a missed bill here, some confusion there, a moment at the doctor’s office that leaves everyone a little uneasy. But the idea that a parent could lose the legal ability to manage their own life rarely feels urgent until it suddenly is.

When a parent loses capacity in New York without a Power of Attorney, a Health Care Proxy, or a trust in place, the consequences aren’t abstract. They’re immediate, they’re expensive, and they fall on the people who love that parent most. This article covers the seven most serious things that can go wrong, and why incapacity planning in New York matters before a crisis arrives.

Key Takeaways

- Being a family member gives you almost no automatic legal authority over a parent’s finances or medical care in New York

- Banks can freeze accounts even when that money is needed to pay for the parent’s own care

- Without a plan, the court steps in through a process called guardianship. It’s public, slow, and often costs tens of thousands of dollars

- Quick fixes like adding a child to a bank account or transferring the house often create bigger problems than they solve

- Medicaid has a five-year look-back rule that can turn last-minute asset moves into financial penalties

- The window to put a legal plan in place closes when a parent loses capacity, and that can happen without warning

1. Your Parent’s Bank Accounts Could Be Frozen

Banks don’t run on family relationships. They run on legal authority. When a parent loses capacity, even a child who has been helping manage their finances for years has no legal right to access an individual bank account without a valid Power of Attorney or a court order. None.

Financial institutions that suspect a customer is experiencing cognitive decline may restrict the account to protect against fraud. The result is that the mortgage doesn’t get paid, the utilities get shut off, and the home care aide goes unpaid, even when the parent has money sitting right there.

Families often try to work around this. Those workarounds tend to create new problems.

| What Families Try | What Actually Happens |

| Adding a child to the bank account | Exposes the parent’s money to the child’s creditors, lawsuits, and divorce proceedings; can trigger Medicaid penalties |

| Sharing online passwords | Violates bank terms of service; creates no record of transactions; can expose the family to fraud liability |

| Adding a child’s name to the deed | Creates serious tax problems when the home is sold; can affect Medicaid eligibility |

A Durable Power of Attorney is a legal document where a parent names someone to manage their finances. It gives one trusted person immediate authority to act. Without it, the family is left waiting for a court to step in.

2. No One May Have the Right to Make Medical Decisions

New York does have a backup system for this. It’s called the Family Health Care Decisions Act, and it gives hospitals a list of people, in order of priority, who can make medical decisions when a patient can no longer speak for themselves. Spouse first, then adult children, and so on.

The catch is that this law only applies in hospitals, nursing homes, and hospice settings. A parent being cared for at home, or living in an assisted living facility that doesn’t meet the legal definition of a nursing home, may fall completely outside its reach. In those situations, family members may have no recognized authority to make decisions, access medical records, or coordinate care.

There’s another problem when multiple adult children are involved. The law places them all at the same level with no way to break a tie. If siblings disagree on a treatment decision, the hospital has to bring in its ethics committee, and everything stalls while the parent waits.

A Health Care Proxy solves this. It’s a simple document where a parent names one person to make medical decisions on their behalf. That person’s authority is clear, it applies in all settings, and there’s no committee required.

3. The Court Steps In Through Guardianship

When a parent loses capacity in New York without any legal documents in place, the family’s only option is to go to court. This process is called guardianship, and it’s governed by Article 81 of New York’s Mental Hygiene Law.

A guardianship case is a formal legal proceeding filed in New York Supreme Court. Everything about it is public. The parent’s medical situation, their finances, and their personal limitations all become part of the court record. The court appoints an independent investigator, called a Court Evaluator, who interviews the family, reviews records, and reports back to the judge.

The process takes months. In New York City, it typically runs four to nine months from filing to having an authorized guardian. And the costs come directly out of the parent’s estate.

| What You’re Paying For | Typical Cost in NYC |

| Your attorney (uncontested case) | $7,500 to $15,000+ |

| Court Evaluator | $2,500 to $10,000 |

| Attorney appointed for your parent | $3,000 to $7,000 |

| Annual bond (insurance for the guardian) | $500 to $5,000+ per year |

| Annual court accountings | $1,000 to $3,000 per year |

| Estimated total (first year, uncontested) | $15,000 to $40,000+ |

A Power of Attorney or trust put in place before any of this happens can keep families out of court entirely.

4. Someone Your Parent Never Met Could End Up in Charge

Most families assume that if guardianship is necessary, a family member will be appointed. That’s not guaranteed.

If siblings are fighting over who should be in charge, or if the court has concerns about the family’s ability to act in the parent’s best interest, a judge can appoint a professional guardian instead. New York maintains a roster of professional guardians for exactly this situation.

A professional guardian is a stranger. They decide where your parent lives, which doctors they see, and who is allowed to visit. Their fees come out of the parent’s estate. And because their authority comes from a court order, not a relationship, the family has very little ability to influence their decisions.

This outcome is more common in New York City than families expect, particularly when siblings are in conflict. A parent’s wishes carry no legal weight if they were never put in writing.

5. The Family Home Can Get Stuck in Legal Limbo

For many New York families, a parent’s home is their most significant asset. It’s often what would fund nursing home care if the parent needs it. When there’s no plan in place, that asset can become extremely difficult to access.

A person who has lost legal capacity cannot sign a contract or a deed. That means the family can’t sell the home, even to pay for care, without court approval. Even a court-appointed guardian doesn’t have automatic authority to sell real estate. They need a separate court order, which means more time, more legal fees, and a home sitting vacant while the process plays out.

Some families respond by trying to transfer the home to a child quickly. That often backfires. A home transferred as a gift during a parent’s lifetime passes to the child at its original purchase price for tax purposes. When the child sells, they owe capital gains taxes on the full increase in value, which on a New York property can be substantial. A home inherited after a parent’s death doesn’t have this problem, because tax law resets the value to the current market price.

A Medicaid Asset Protection Trust (MAPT), set up while the parent still has legal capacity, can protect the home from nursing home costs and preserve the tax benefit for the family. That option largely disappears once capacity is gone.

6. Medicaid Planning Gets Much Harder

Nursing home care in New York City costs between $15,000 and $20,000 per month. Most families can’t cover that for long. Medicaid pays for long-term care for people who qualify, but qualifying has strict rules.

One of those rules is the five-year look-back. When someone applies for Medicaid to cover nursing home care, the government reviews every financial transaction they made in the previous five years. Any money transferred to family members, any assets moved out of their name, anything that looks like an attempt to qualify for benefits: all of it can result in a penalty period where Medicaid won’t pay, even if the person genuinely needs care.

Families who try to protect assets after a parent is already declining often trigger exactly this penalty without realizing it. The right time to do Medicaid planning is before the crisis, while the parent still has the legal capacity to sign documents. Once that capacity is gone, the available options shrink considerably, and every move requires additional court approval.

7. Family Relationships Can Break Down Permanently

The legal and financial problems that come with unplanned incapacity are serious. What’s harder to put a number on is what it does to families.

When no one has been given clear legal authority, siblings tend to fill the vacuum by competing for control. One child manages the money and the others grow suspicious. Another pushes for one type of care while a third insists on something different. Under New York’s guardianship law, any “interested person” can get involved in court proceedings, which means old family tensions often resurface and play out publicly, paid for by the parent’s estate.

Contested guardianship cases in New York City can cost more than $100,000 in combined legal fees. Courts that can’t identify a suitable family member sometimes appoint a professional stranger instead. The damage done to sibling relationships during these proceedings rarely heals completely.

It’s also the most preventable outcome on this list. Clear legal documents, signed while a parent still has capacity, take the ambiguity out of who decides. That protects the parent. It also protects the family.

What Incapacity Planning in New York Actually Looks Like

Every problem in this article comes from the same place: no legal plan existed when capacity was lost. The right documents, drafted properly and put in place in time, prevent most of these outcomes.

| Document | What It Does |

| Durable Power of Attorney | Names someone to manage finances; keeps banks accessible; avoids guardianship of property |

| Health Care Proxy | Names one person to make medical decisions; applies in all settings; eliminates the need for court involvement |

| Living Will | Records the parent’s wishes for end-of-life care; gives the Health Care agent clear guidance |

| Revocable Living Trust | Holds assets so a successor can manage them immediately, without court involvement |

| Medicaid Asset Protection Trust | Protects assets from nursing home costs while starting the five-year Medicaid clock |

In New York, a parent can still sign these documents even after an early diagnosis, as long as they still understand what they’re agreeing to. That window can close faster than families expect. Getting a plan in place while it’s still open is almost always the right move.

How Fisher Stone Can Help

At Fisher Stone, we help New York families put plans in place before a crisis forces them into court. That means Powers of Attorney that hold up when banks push back, Health Care Proxies and Living Wills that clearly reflect what your family wants, and trust structures built around your specific situation and long-term care concerns.

If your family is dealing with a parent’s declining health, or if you want to make sure you’re prepared before something changes, contact Fisher Stone to schedule a consultation.

What happens to my parent’s bank accounts if they lose capacity without a Power of Attorney in New York?

Without a Power of Attorney, no family member has the legal right to access a parent’s individual bank accounts, regardless of how involved they are in that parent’s life. Banks are legally prohibited from giving access without proper authorization. In practice, this means accounts get frozen at exactly the moment families need them most — to pay for care, cover bills, or handle day-to-day expenses. The only ways to regain access are a valid Power of Attorney or a court order through New York’s guardianship process, which takes months and costs thousands of dollars.

Can I make medical decisions for my parent in New York without a Health Care Proxy?

New York’s Family Health Care Decisions Act allows certain family members to make medical decisions for an incapacitated parent in hospitals and nursing homes, even without a Health Care Proxy. But this law has real limits. It doesn’t apply to care given at home or in most assisted living settings. And if there are multiple adult children, they all have equal standing with no built-in tiebreaker, which can lead to gridlock at the hospital. A Health Care Proxy removes all of that uncertainty by naming one person with clear authority that applies in every setting.

How much does guardianship cost in New York?

In an uncontested case in New York City, total costs in the first year commonly run between $15,000 and $40,000, covering the petitioner’s attorney, the Court Evaluator, and the attorney appointed for the parent. All of these fees come out of the parent’s estate. Contested cases, where family members disagree or someone fights the petition, can push combined fees well past $100,000. There are also ongoing annual costs for as long as the guardianship lasts, including a fiduciary bond and annual court accountings.

Is it too late to do Medicaid planning after a parent is diagnosed with dementia?

Not necessarily, but the options get much narrower. Medicaid’s five-year look-back rule means that assets transferred after a diagnosis — and within five years of applying for benefits — can result in a penalty period where Medicaid won’t pay. The most effective planning tools, including a Medicaid Asset Protection Trust, need to be set up while the parent still has legal capacity to sign documents. A parent in the early stages of a diagnosis may still qualify. The sooner you speak with an elder law attorney, the more options the family has.

Can my parent still sign a Power of Attorney if they have early-stage dementia?

Possibly, yes. New York law doesn’t automatically disqualify someone from signing legal documents just because they have a dementia diagnosis. What matters is whether, at the time of signing, your parent understands what the document is, who they’re naming, and what that person will be allowed to do on their behalf. A parent with early-stage dementia may still meet that standard. An elder law attorney can assess the situation and, if capacity is borderline, work with the parent’s doctor to document it properly. Acting while this window is still open is almost always the right call.